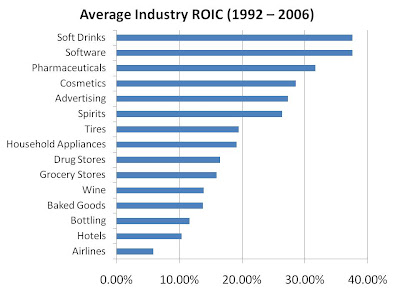

Harvard Professor Michael Porter, using data from Standard and Poor's as well as Compustat, has calculated the profitabilites of various industries over the 1992-2006 period, some of which are shown below:

Clearly, there is high variability in returns on capital by industry. Average industry ROIC in the US was calculated at 14.9% by Porter, demonstrating that some industries are clearly extremely profitable, while others destroy capital.

Does this mean you shouldn't own a company whose industry returns fall below the average ROIC? Absolutely not! Within industries, returns may also be highly variable, in the case where one or two companies have differentiated themselves or are low-cost producers that generate consistent industry-beating returns. Furthermore, even companies with meager returns can trade at such large discounts to book that returns on the market price of equity are quite high. But you may still want to stay away from the airline industry!

2 comments:

Very interesting list and quite eye opening.

It'd be interesting to see where some of the higher growth industries fit in there as I would expect to see an inverse relationship between growth and equity returns.

This is interesting - but what be VERY interesting if you followed this up with a post comparing industry equity RETURNS vs. invested capital returns... (more or less what the reader above state)

Post a Comment