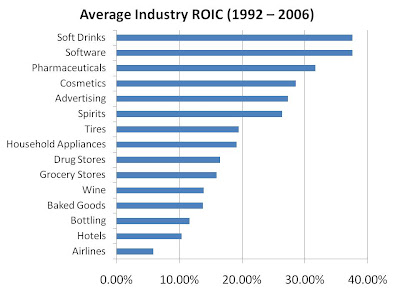

Harvard Professor Michael Porter, using data from Standard and Poor's as well as Compustat, has calculated the profitabilites of various industries over the 1992-2006 period, some of which are shown below:

Clearly, there is high variability in returns on capital by industry. Average industry ROIC in the US was calculated at 14.9% by Porter, demonstrating that some industries are clearly extremely profitable, while others destroy capital.

Does this mean you shouldn't own a company whose industry returns fall below the average ROIC? Absolutely not! Within industries, returns may also be highly variable, in the case where one or two companies have differentiated themselves or are low-cost producers that generate consistent industry-beating returns. Furthermore, even companies with meager returns can trade at such large discounts to book that returns on the market price of equity are quite high. But you may still want to stay away from the airline industry!

9 comments:

Can you point us to the source of that study? Thanks, Paul

Hello, just curious could post a link to the porter reaserch.

I am interested to see if there was control for survivorship bias in the presentation as this would produce even more pronounced variance in returns.

thank you.

Ditto - link to Porter research?

Hi guys,

It looks like it's available here.

Hey all,

Why do you think companies have ROIC to begin with? Why isn't the business world perfectly efficient thereby creating no net income? Isn't most ROIC negative given the fact that most businesses eventually go bankrupt or fail to exist? This includes only operating businesses. If you took all capitial invested in the business world do you think it would be 0 or even negative? Thanks.

Also, what do you guys think the ROIC is on a rental property company? I could imagine it being very low. Ie the spreads between NOI - Debt payments are really low in comparison to a total value of property invested. I am sure the property management company's profit margins are way higher and less assets. Almost like a CPA firm.

Some industries are very capital light, sometimes completely so, and therefore ROIC is meaningless for them.

If an exceptional oil driller has 40% ROIC margins, it can probably go spend money buying additional oil rigs and earn close to 40% on the money it just spent. A software or internet company, like EBAY, might have 40% margins, but spending money on acquiring new assets won't expand their business or earnings at all. It just doesn't require much capital, and doesn't have the opportunity to put new cash to work earning that 40% ROIC.

The best way to expand their business by spending money, is perhaps through research or marketing, neither of which ROIC measures.

So although this study is interesting, the inclusion of capital light industries can be misleading.

-Hester

JUST BECAUSE YOU HAVE A HIGH ROIC BECAUSE YOU DONT HAVE A LOT OF C!!! Doesn't mean anything. In fact, that is good to be an investor in a company that does not need a lot of C!!!! Especially, when they have competitive advantages. Thats the hole point of the equation.

Anonymous,

Here is my answers to some of your questions. I'm not entirely sure that I'm right so hopefully someone will correct me where I'm wrong...

Anonymous: "Why do you think companies have ROIC to begin with? Why isn't the business world perfectly efficient thereby creating no net income?"

If every business generated zero net income, it would make no sense. After all, why would anyone invest or create a new business if there is no profit to be had. Owners will need to be compensated for risking their capital so net income can never be zero (except in some special cases).

Anonymous: "Isn't most ROIC negative given the fact that most businesses eventually go bankrupt or fail to exist? This includes only operating businesses. If you took all capitial invested in the business world do you think it would be 0 or even negative?"

Nope. Even if companies go bankrupt, the return should still be positive since profits generated over the life cycle of a firm is greater than any loss upon bankruptcy.

For example, you may invest, say, $2 million initially but earn $1 million per year for 20 years. Even if the company goes bankrupt in 20 years and you lose the $2 million investment (say liquidation value is zero), you will still have earned a positive profit over its full life.

ROIC (or ROE) should not be negative except for a few failing firms or some industries that are struggling. So, it's probably possible for ROIC to be negative for industries facing decline (I'm not sure and am guessing on this). I supposed you may also see negative ROIC if the country is suffering (say during a war or a total collapse or something).

(On another note...not sure about the property rental company question you asked.)

HESTER: "If an exceptional oil driller has 40% ROIC margins, it can probably go spend money buying additional oil rigs and earn close to 40% on the money it just spent. A software or internet company, like EBAY, might have 40% margins, but spending money on acquiring new assets won't expand their business or earnings at all. It just doesn't require much capital, and doesn't have the opportunity to put new cash to work earning that 40% ROIC."

Hester, I'm not sure I understand this. Are you assuming that the asset-light company will invest in projects earning less than 40% ROIC (in this example)? If you are saying that, I don't think it is necessarily true. If you look at a company like Microsoft, it is arguably an asset-light company for a company of its size yet it continuously re-invests profits and its ROIC hasn't really declined in the last decade (it actually went up; refer to last line here).

The way I look at it, unless you are absolutely certain that an asset-light company will re-invest profits into projects with declining profitability, there is no reason to distinguish asset-light companies from asset-heavy ones; it doesn't matter. In fact, as someone above suggests, an asset-light company is way better to own because it is more capital efficient.

Post a Comment